Table of Contents

Stablecoin Guide- ➔ Introduction: The Digital Dollar Promise

- ➔ 1. Types of Stablecoins: Fiat, Crypto & Algorithmic

- ➔ Visual Insights: Market Trends & De-Peg Events

- ➔ 2. Real-World Use Cases: Payments & DeFi

- ➔ 3. Safety Concerns: Reserve Transparency & Run Risk

- ➔ 4. Regulatory Outlook: The IMF & Central Banks

- ➔ Who Should (and Shouldn’t) Use Stablecoins?

- ➔ Stablecoin FAQ: Security & Strategy

- ➔ Conclusion: Managing Digital Stability

Introduction

Imagine a digital dollar that moves as fast as a text message, available 24/7 worldwide, and aims to maintain a steady value despite the volatility of traditional cryptocurrencies. This is the promise of stablecoins, a category of digital assets designed to combine the speed and accessibility of crypto with the price stability of traditional money like the U.S. dollar, and sometimes even commodities such as gold.

Stablecoins are rapidly gaining adoption, not only among crypto traders but also within mainstream finance. They are widely used for payments, trading, cross-border transfers, and decentralized finance (DeFi) applications. However, beneath their reassuring name lies an important question: are stablecoins truly safe, or are they only “stable” under ideal conditions?

To understand stablecoins, you must examine how they maintain their value, what assets back them, and the risks involved. Some are supported by real-world reserves such as cash or government securities, while others rely on crypto collateral or complex algorithmic mechanisms. History has shown that confidence is critical — when trust weakens, even assets labeled as “stable” can lose their peg, as demonstrated by the collapse of TerraUSD.

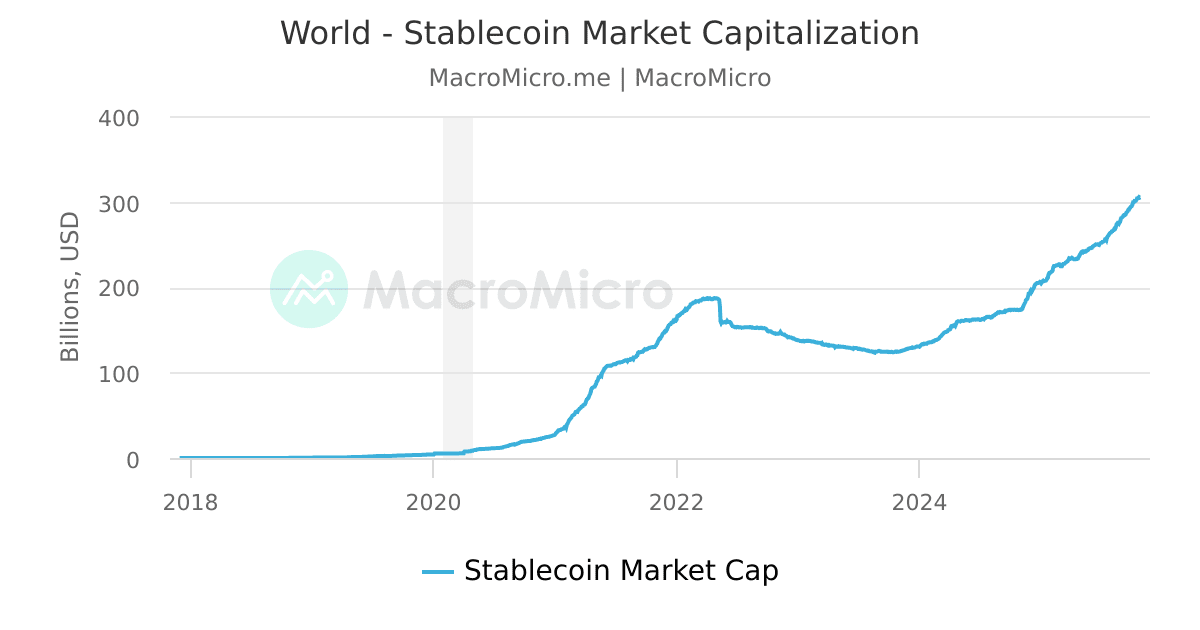

Stablecoins now represent over $300 billion in circulating value, reflecting their expanding role in global payments, trading, and decentralized finance.

In this guide, we will explore the different types of stablecoins, how they function, their real-world applications, and the key safety concerns investors and users should consider. By the end, you will have a clear, balanced understanding of what “stable” truly means in the evolving world of digital money.

1. Types of Stablecoins

Stablecoins are not all created equal. How they maintain their value—and how safe they are—depends on what backs them and the mechanism keeping their price stable. Broadly, there are three main types: fiat-backed, crypto-backed, and algorithmic stablecoins. Each comes with unique benefits, risks, and trade-offs.

Fiat-Backed Stablecoins

Examples: USDT (Tether), USDC (USD Coin), BUSD

How They Work:

Fiat-backed stablecoins are pegged 1:1 to a traditional currency, usually the US dollar. The issuer claims that for every coin in circulation, an equivalent dollar (or equivalent asset) is held in reserve—often in bank accounts, cash, or short-term securities.

Pros:

-

Simplicity: Easy to understand; value is tied directly to real-world money.

-

Stability: Less volatile than other cryptocurrencies.

-

Liquidity: Widely accepted for trading and payments.

Cons:

-

Trust Required: Users must believe the issuer actually holds the reserves.

-

Centralization: A single entity controls the coin and can freeze transactions if required.

-

Regulatory Risk: Subject to audits, banking regulations, and government oversight.

Crypto-Backed Stablecoins

Examples: DAI (MakerDAO), sUSD

How They Work:

Crypto-backed stablecoins are secured with other cryptocurrencies, such as Ethereum (ETH). Because crypto prices are volatile, these coins are often over-collateralized—for example, $150 worth of ETH might be locked to mint $100 of DAI. Smart contracts automatically manage liquidations to maintain stability.

Pros:

-

Decentralization: Operates on blockchain protocols without relying on a single issuer.

-

Transparency: Collateral is visible on-chain for anyone to verify.

-

Resilience: Cannot be arbitrarily frozen by a central authority.

Cons:

-

Complexity: Can be confusing for beginners.

-

Volatility Risk: Rapid drops in collateral value can trigger forced liquidations.

-

Capital Inefficiency: Over-collateralization ties up more assets than fiat-backed coins.

Algorithmic Stablecoins

Examples: TerraUSD (UST, now defunct), Ampleforth

How They Work:

Algorithmic stablecoins use computer algorithms and market incentives to maintain a peg—without holding real-world reserves. If the price drops below $1, the protocol reduces supply; if it rises above $1, it increases supply.

Pros:

-

No Reserves Needed: Operates independently of banks or collateral.

-

Fully On-Chain: Autonomous and theoretically decentralized.

Cons:

-

Fragility: Relies heavily on market confidence and correct incentive structures.

-

High Risk of Collapse: If confidence fails, the peg can break rapidly—as seen with TerraUSD.

Experimental: Few algorithmic stablecoins have survived long-term.

Comparison of Stablecoin Types

| Type | Backing | Example | Key Advantage | Main Risk |

|---|---|---|---|---|

| Fiat-Backed | Traditional currency | USDC | Simple, stable | Centralized, trust-based |

| Crypto-Backed | Cryptocurrency | DAI | Decentralized, transparent | Volatile, complex |

| Algorithmic | None (algorithm) | UST | No reserves, fully on-chain | Fragile, experimental |

3. Safety Concerns of Stablecoins

Despite their name, stablecoins are not risk-free. Their promise of stability depends on complex mechanisms, reserves, and trust. Understanding the potential pitfalls is crucial before using or investing in them.

Reserve Transparency

For fiat-backed stablecoins, the main question is simple: Are they really backed 1:1 by dollars or equivalent assets?

-

Tether (USDT): For years, Tether claimed to be fully backed by dollars, but investigations revealed that some reserves were held in commercial paper or other riskier assets.

-

USD Coin (USDC): USDC publishes regular audits showing its reserves, but users must trust both the issuer and the auditor.

Risk: If reserves are insufficient, a sudden wave of redemptions could reveal a shortfall, causing the coin to lose its peg.

Users must also stay alert to crypto scams and fraud risks, which can undermine trust even in coins marketed as stable.

Run Risk

Much like a traditional bank run, stablecoins can face a loss of confidence, prompting holders to redeem en masse for real dollars.

-

Consequence: If the issuer cannot fulfill all redemptions, the stablecoin can crash below $1, resulting in significant losses for users.

-

Why it matters: Even coins with strong backing can experience rapid price drops during panic, especially in volatile markets. Recent brief de-peg incidents in 2025–2026 have reinforced that even well-established stablecoins remain sensitive to market confidence.

For example, during the Silicon Valley Bank crisis in March 2023, USDC briefly fell below $1 after part of its reserves were temporarily inaccessible. Although the peg was restored, the event showed how quickly market confidence can weaken — even in well-established stablecoins.

Regulatory Uncertainty

Stablecoins exist in a legal gray area. Governments and regulators worldwide are still defining how they should be classified, whether as securities, payment instruments, or something else.

-

Potential Impact: Authorities could freeze accounts, restrict operations, or impose new compliance requirements.

-

Current Trends:

-

The US SEC and CFTC have increased scrutiny.

-

The EU introduced the MiCA framework, regulating stablecoins under clear guidelines.

-

-

Takeaway: Regulatory changes can affect both usability and the perceived safety of stablecoins.

Algorithmic Failures: Lessons from TerraUSD

Algorithmic stablecoins, which rely on market mechanisms instead of reserves, can be particularly fragile.

-

Case Study: TerraUSD (UST) in 2022 collapsed when its algorithmic system failed. Confidence faltered, LUNA’s value plummeted, and over $40 billion in market value vanished within days.

-

Lesson: Without robust backing or trust in the mechanism, even coins marketed as “stable” can fail catastrophically.

Smart Contract and Cybersecurity Risk

Even decentralized stablecoins face risks from bugs or hacks, making it essential to protect your portfolio from cyber risks:

-

Vulnerabilities in smart contracts can allow attackers to drain funds or manipulate the system.

-

Users must rely on the code and the platform’s security measures rather than a central institution.

No stablecoin is completely risk-free. Even the most reputable stablecoins rely on trust — whether in the issuer, the collateral, or the code itself. Understanding the mechanisms and risks is the first step toward using them safely.

4. Regulatory Outlook

The rapid growth of stablecoins — from roughly $5 billion in 2019 to over $300 billion by 2026 — has drawn significant attention from regulators worldwide. Their influence on payments, trading, and financial markets means governments are taking a closer look. In the United States, new federal frameworks introduced in 2025–2026 have increased reserve transparency requirements and strengthened oversight of large stablecoin issuers. Meanwhile, the European Union’s MiCA framework has begun phased implementation, establishing clearer compliance standards for asset-referenced tokens.

Concerns from Central Banks and the IMF

Global financial authorities worry that unchecked stablecoin growth could threaten financial stability:

-

Run Risk: A sudden loss of confidence could trigger mass redemptions, affecting banks and markets.

-

Contagion: Problems with one large stablecoin could spill over into other financial sectors.

-

Shadow Banking: Stablecoins can enable bank-like activities outside traditional regulatory oversight, creating systemic risk.

The International Monetary Fund (IMF) and several central banks have flagged these issues, urging careful regulation to protect consumers and the financial system.

Likely Regulatory Responses

To mitigate risks, governments are proposing a range of measures:

• Stricter Audits and Reserve Requirements: Issuers may be required to hold high-quality, liquid assets and undergo regular, independent audits.

• Licensing and Supervision: Some jurisdictions require stablecoin issuers to register as money transmitters or obtain bank charters.

• Limits on Algorithmic Models: Regulators are increasingly skeptical of uncollateralized, algorithmic stablecoins due to their inherent fragility.

• Competition from Central Bank Digital Currencies (CBDCs): Governments are developing their own digital currencies, which could offer the same speed and convenience as stablecoins — but with official backing and regulatory oversight.

Who Should (and Shouldn’t) Use Stablecoins?

Stablecoins can be useful for:

-

Traders who need temporary protection from crypto volatility

-

Freelancers and businesses handling cross-border payments

-

DeFi users participating in lending or liquidity pools

However, they may not be ideal for:

-

Long-term wealth storage without understanding issuer risk

-

Investors seeking guaranteed safety

-

Users unwilling to monitor regulatory or market developments

Like any financial tool, stablecoins are best used with clear purpose and risk awareness.

Stablecoin FAQ: Security & Strategy

Everything you need to know about digital price stability

1. If a stablecoin is pegged to the Dollar, why does the price sometimes fluctuate? ▼

2. What is the difference between USDT and USDC? ▼

3. Is it safe to hold my life savings in stablecoins? ▼

4. How do I verify if a stablecoin is actually backed by reserves? ▼

5. Can the government freeze my stablecoins? ▼

6. Why would anyone use an algorithmic stablecoin after the Terra collapse? ▼

7. Will Central Bank Digital Currencies (CBDCs) replace stablecoins? ▼

Conclusion

Stablecoins are redefining the way money moves in the digital age. They offer instant, low-cost, and borderless transactions, serve as a temporary safe haven for crypto traders, and power innovative financial products within decentralized finance (DeFi).

But “stable” does not automatically mean “safe.” Their security depends on:

• Transparency: Are reserves or collateral clearly documented and independently audited?

• Regulation: Are issuers operating within legal frameworks designed to protect users?

• Trust: Is the system, whether centralized, crypto-backed, or algorithmic, reliable and resilient during market stress?

Key Takeaways:

• Understand the type of stablecoin and how it maintains its value.

• Before committing funds, always conduct due diligence when evaluating cryptocurrency projects to ensure transparency and reliability.

• Monitor regulatory developments and overall market confidence.

• Be cautious with experimental or high-yield coins, as they often carry significantly higher risk.

As the market matures, stablecoins will likely become more transparent and better regulated. Still, users should never assume that “stable” means risk-free. In digital finance, stability is engineered, maintained, and constantly tested. Stay informed, use reputable platforms, and diversify your exposure to protect your funds.

No comments:

Post a Comment

We welcome thoughtful and constructive comments. Please ensure your feedback is respectful and relevant to the topic discussed. Comments may be moderated.